An unprecedented number of U.S. factories were under construction in 2023. The U.S. needs to keep it up.

There was an American factory boom in 2023.

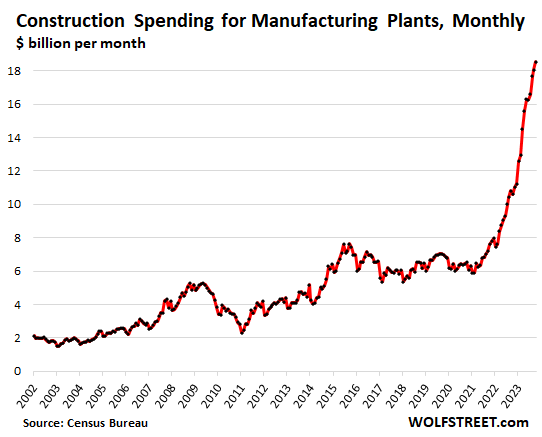

A real big one. We’re still waiting on the full number, but construction on manufacturing plants topped approximately $200 billion in private spending this year, which was approximately $80 billion more than in 2022. That big jump was due, in part, to the huge industrial policies being enacted by Washington, and ground being subsequentially broken on enormous EV battery plants and semiconductor chip fabs – industries that were targeted for growth by the Inflation Reduction Act and the CHIPS Act, respectively.

But even though there was a huge jump in spending on production facilities for these specialized electronic goods in 2023, manufacturing spending was already accelerating since the Covid-19 pandemic slowed in 2021. From that year to 2022, manufacturing construction spending across the U.S. increased by more than $20 billion, a substantial sum on its own.

So it begs the question: What stepped on the gas in 2021? What caused it?

A zeitgeist shift? A new era of thinking? A sea change. What happened was globalization retreated a little bit. This was in large part because bilateral relations between the countries with the two largest national economies – the United States and China – grew rocky during the Trump administration, which unsettled the business environment. While the two ratcheted up tariffs on each others’ products, corporate titans grew a little uncertain of the wisdom in importing everything they sell in the U.S. market from factories across the ocean, from a country with a potentially hostile government. Perhaps, they thought, they should locate production a little closer to the consumers they were targeting.

And then the pandemic hit, and production plans really started to move. The Infrastructure Investment and Jobs Act and its strong Buy America rules came online in late 2021, spurring investment in things like factories that make broadband cable to expand fast Internet access. And then the IRA and the CHIPS Act showed up in late 2022, and now construction activity is like a snowball barreling downhill.

Employment hasn’t kept pace. Despite manufacturing construction getting into gear, manufacturing employment in 2023 was essentially flat, as inflation was high and consumers started spending more on services (like going on vacation) more post-pandemic.

But all this factory construction is going to beget more factory jobs, as the labor market will shift to fill these open positions. And, what’s more, not all the inducements allocated in these big industrial policies has been allocated yet. More is likely coming, and that means 2024 very likely could see even more elevated spending on manufacturing construction. If lawmakers really want manufacturing jobs that offshored to Asia 20 and 30 years ago to return in force, they should be accelerating those industrial policy allocations while emphasizing the domestic production rules that underpin them, and keep an eye out for vigilant on the trade front so that newly made investments aren’t completely swamped by production overcapacity in, say, the Chinese solar panel industry.

Globalization uncertainty + pandemic shock + industrial policy = an American factory boom.